Last year marked the 25th anniversary for Upfront Ventures and what a year it was. 2021 saw phenomenal returns for our industry and it topped off more than a decade of unprecedented VC growth.

The industry has obviously changed enormously in 2022 but in many ways it feels like a “return to normal” that we have seen many times in our industry. Yves Sisteron, Stuart Lander & I (depicted in the photo below) have worked together for more than 22 years now and that has taken us through many cycles of market enthusiasm & panic. We’ve also worked with our Partner, Dana Kibler who is also our CFO for nearly 20 years.

We believe this consistency in leadership and intuition for where the markets were going in the heady days of 2019–2021 helped us to stay sane in a world that momentarily seemed to have lost its mind and since we have new capital to deploy in the years ahead perhaps I can offer some insights into where we think value will be derived.

Focus on Cash

While the headlines in 2020 & 2021 touted many massive fundraising events and heady valuations, we believed that for savvy investors it also represented an opportunity for real financial gains.

Since 2021, Upfront returned more than $600 million to LPs and returned more than $1 billion since 2018.

Considering that many of our funds are in the $200–300 million range, these returns were more meaningful than if we had raised billion dollar funds. We remain confident in the long-term trend that software enables and the value accrued to disruptive startups; we also recognized that in a strong market it is important to ring the cash register and this doesn’t come without a concentrated effort to do so.

Obviously the funding environment has changed considerably in 2022 but as early-stage investors our daily jobs stay largely unchanged. And while over the past few years we have been laser-focused on cash returns, we are equally planting seeds for our next 10–15 years of returns by actively investing in today’s market.

We are excited to share the news that we have raised $650 million across three vehicles to allow us to continue making investments for many years ahead.

We are proud to announce the close of our 7th early-stage fund with $280 million to invest in seed and early stage founders.

Alongside Upfront VII we are also now deploying our third growth-stage fund, which has $200 million in commitments and our Continuation Fund of more than $175 million.

What do you do with a $650 million platform?

A question I often hear is “how is Upfront changing given the current market?” The answer is: not much. In the past decade we have remained consistent, investing in 12–15 companies per year at the earliest stages of their formation with a median first check size of approximately $3 million.

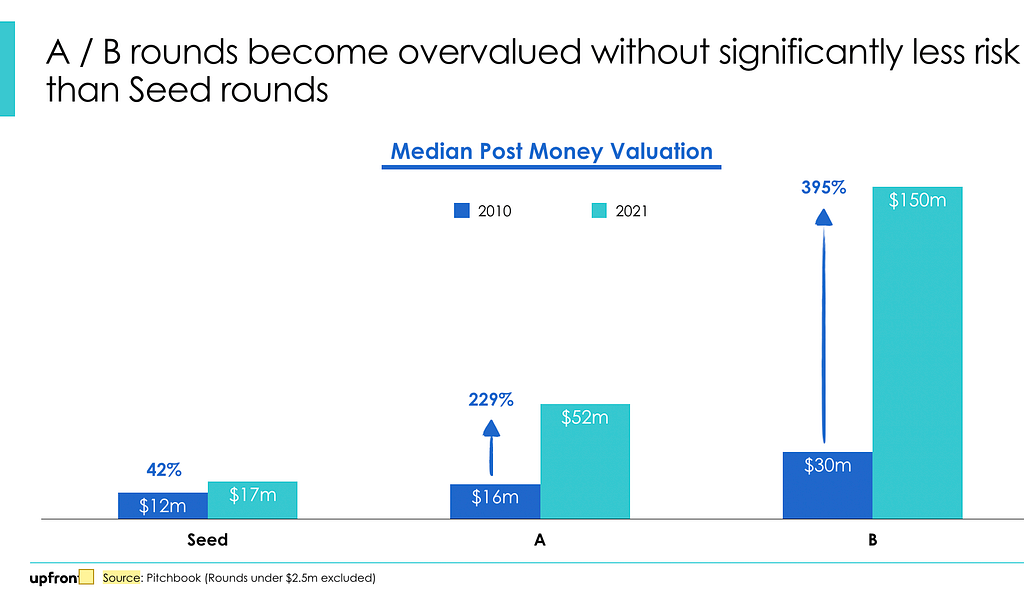

If I look back to the beginning of the current tech boom which started around 2009, we often wrote a $3–5 million check and this was called an “A round” and 12 years later in an over-capitalized market this became known as a “Seed Round” but in truth what we do hasn’t changed much at all.

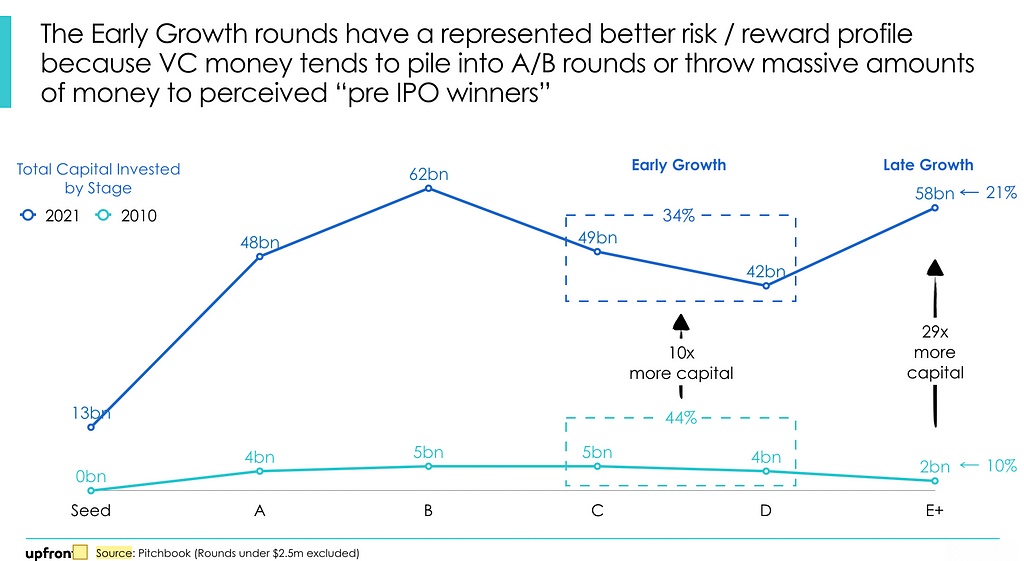

And if you look at the above data you can see why Upfront decided to stay focused on the Seed Market rather than raise larger funds and try and compete for A/B round deals. As money poured into our industry, it encouraged many VCs to write $20–30 million checks at increasingly higher and higher valuations where it is unlikely that they had substantively more proof of company traction or success.

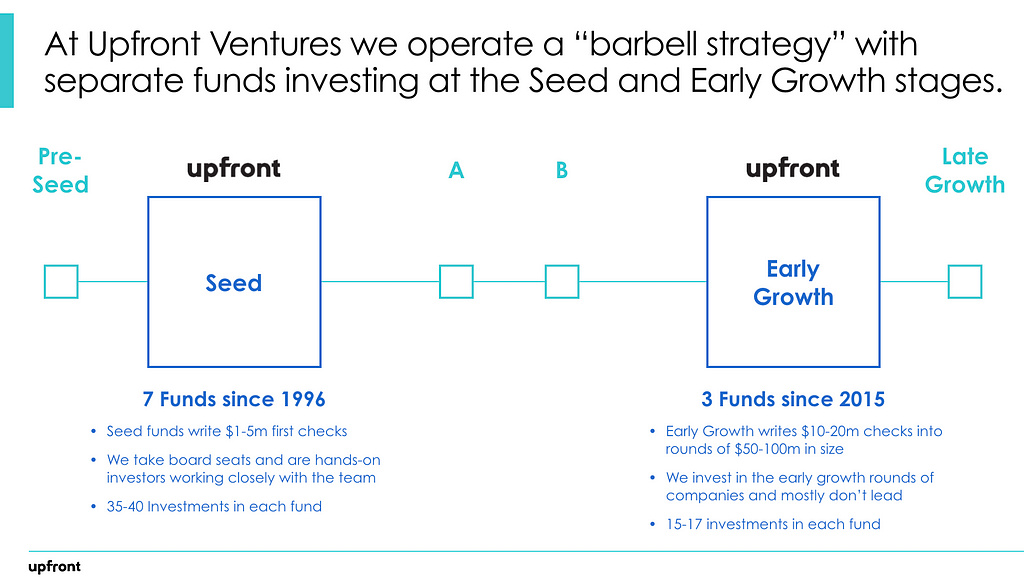

Some investors may have succeeded with this strategy but at Upfront we decided to stay in our lane. In fact, we published our strategy some time ago and announced we were moving to a “barbell strategy” of funding at the Seed level, mostly avoiding the A/B rounds and then increasing our investments in the earliest phases of technology growth.

When we get involved in Seed investments we usually represent 60–80% in one of the first institutional rounds of capital, we almost always take board seats and then we serve these founders over the course of a decade or longer. In our best-performing companies we often write follow-on checks totaling up to $10–15 million out of our early-stage fund.

Beginning in 2015 we realized that the best companies were staying private for longer so we started raising Growth Vehicles that could invest in our portfolio companies as they got bigger but could also invest in other companies that we had missed at the earliest stages and this meant deploying $40–60 million in some of our highest-conviction companies.

Size Matters

But why have we decided to run separate funds for Seed and for Early Growth and why didn’t we just lump it all into one fund and invest out of just one vehicle? That was a question I had been asked by LPs in 2015 when we began our Early Growth program.

In short,

In Venture Capital, Size Matters

Size matters for a few reasons.

As a starting point we believe it is easier to consistently return multiples of capital when you aren’t deploying billions of dollars in a single fund as Fred Wilson has articulated consistently in his posts on “small ball” and small partnerships. Like USV we are usually investing in our Seed fund when teams are fewer than 10 employees, have ideas that are “out there” and where we plan to be actively engaged for a decade or longer. In fact, I am still active on two boards where I first invested in 2009.

The other argument I made to LPs at the time was that if we combined $650 million or more into a single fund it would mean that writing a $3–4 million would feel too small to each individual investor to be important and yet that’s the amount of capital we believed many seed-stage companies needed. I saw this at some of my peers’ firms where increasingly they were writing $10+ million checks out of very large funds and not even taking board seats. I think somehow the larger funds desensitized some investors around check sizes and incentivized them to search for places to deploy $50 million or more.

By contrast, our most recent Early Growth fund is $200 million and we seek to write $10–15 million into rounds that have $25–75 million in capital including other investment firms and each and every commitment really matters to that fund.

For Upfront, constrained size and extreme team focus has mattered.

But What Has Changed at Upfront?

What has shifted for Upfront in the past decade has been our sector focus. Over the past ten years we have focused on what we believe will be the most important trends of the next several decades rather than concentrating on what has driven returns in the past 10 years. We believe that to drive returns in venture capital, you have to get three things correct:

- You need to be right about the technology trends are going to drive society

- You need to be right about the timing, which is 3–5 years before a trend (being too early is the same as being wrong & if you’re too late you often overpay and don’t drive returns)

- You need to back the winning team

Getting all three correct is why it is very difficult to be excellent at venture capital.

What that means to us at Upfront today and moving forward with Upfront VII and Growth III is a deeper concentration on those categories where we anticipate the most growth, the most value creation, and the biggest impact, most specifically:

- Healthcare & Applied Biology

- Defense Technologies

- Computer Vision

- Ag Tech & Sustainability

- Fintech

- Consumerization of Enterprise Software

- Gaming Infrastructure

None of these categories are new for us, but with this fund we are doubling down on our areas of enthusiasm and expertise.

How do we plan to do it?

Venture capital is a talent game, which starts with the team that’s inside Upfront. The Upfront VII and Growth teams are made up of 10 partners: 6 leading investment activities & 4 supporting portfolio companies including Talent, Marketing, Finance & Operations.

Most who know Upfront are aware that we are based out of Los Angeles where we deploy ~40% of our capital but as I like to point out, that means the majority of our capital is deployed outside of LA! And the number one destination outside of LA is San Francisco.

So while some investors have announced they’re moving to Austin or Miami we have actually been increasing our investments in San Francisco, opening an office with 7 investment professionals that we’ve been slowly building over the past few years. It is led by two partners: Aditi Maliwal on the Seed Investment Team who also leads our Fintech practice and Seksom Suriyapa on the Growth Team who joined Upfront in 2021 after most recently leading Corp Dev at Twitter (and before that at Success Factors and Akamai).

The more things change, the more they stay the same.

So while our investing platform has grown in both size and focus, and while the market is transitioning into a new and potentially more challenging reality (at least for a few years) — in the most important ways, Upfront remains committed to what we’ve always focused on.

We believe in being active partners with our portfolio, working alongside founders and executive teams in both good times and in more challenging times. When we invest, we commit to being long-term partners to our portfolio and we take that responsibility seriously.

We have strong views, take strong positions, and operate from a place of strong conviction when we invest. Every founder in our portfolio is there because an Upfront partner had unwavering belief in their potential and did whatever it took to get the deal done.

We are so thankful to the LPs who continue to trust us with their capital, time and conviction. We feel blessed to work alongside startup founders who are really rising to the challenge of the more difficult funding environment. Thank you to everybody in the community who has supported us all these years. We will continue to work hard to make you all proud.

Thank you, thank you, thank you.

Upfront Ventures Raises > $650 Million for Startups and Returns > $600 Million to LPs was originally published in Both Sides of the Table on Medium, where people are continuing the conversation by highlighting and responding to this story.

Originally published on Both Sides of the Table: Original article